Ian Lance, Co-Portfolio Manager

This year, Temple Bar celebrates its centenary. One hundred years is a long time in any walk of life – long enough to have witnessed the Wall Street Crash, two world wars, the dot-com bubble, a global financial crisis, a pandemic, and today, fresh conflict in the Middle East. In our view, through all of it, the principles first set down by Benjamin Graham, the father of value investing – that paying less than something is worth is the most reliable path to long-term investment returns – have proved their worth. They represent the foundation of how we manage the trust today.

To mark the occasion, it seems a good moment to ask what a century of evidence actually tells us about the discipline. The answer is rather compelling.

Proof, not promise – what a century of data shows

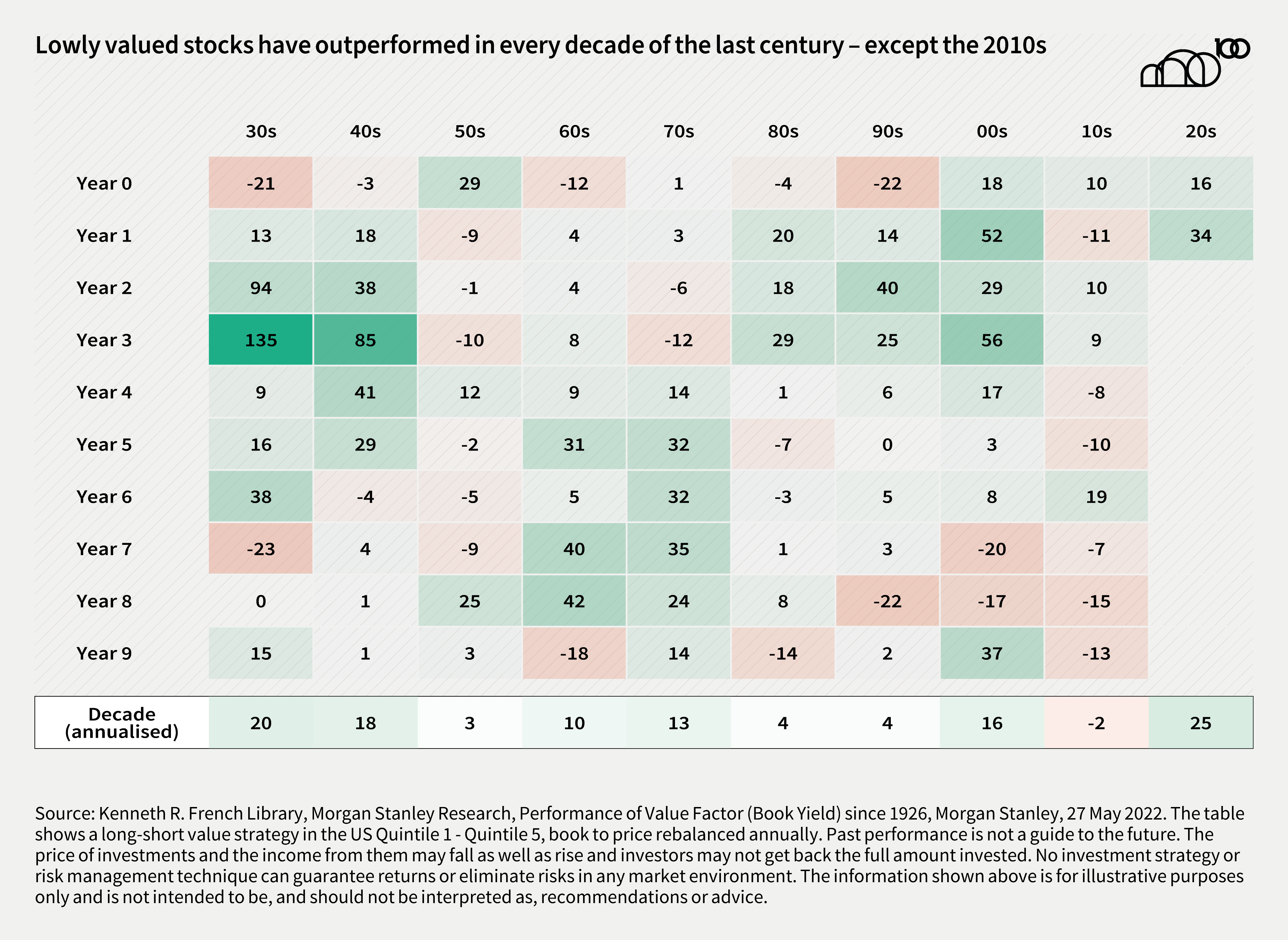

The chart below tracks the performance of lowly valued stocks relative to more expensive ones across every complete decade since the 1920s. The picture it paints is striking – in nine out of ten decades, value investing has outperformed. The one exception – the 2010s – is the subject we will return to shortly.

What the data shows is not that value investing works every quarter, or every year. It does not. What it shows is something more durable and, we would argue, more useful – that over a long enough time horizon, the discipline of buying assets priced below their intrinsic worth has been rewarded with remarkable consistency. Crashes, recessions, wars, bubbles – none of these has been sufficient to break that relationship. Only one decade in a century has managed it, and as we will explain, the conditions that produced that exception were historically unusual.

This conclusion is also supported by the UBS Global Investment Returns Yearbook – one of the most authoritative long-run studies of financial market returns, with data stretching back to 1900. Its long-term factor research shows value delivering positive premiums across most decades in both the US and UK, with the 2010s as the clear outlier. It is reassuring, if not surprising, to find the evidence from independent academic studies pointing to exactly the same conclusion.

Price, value, and the gap in between

Why should this be? The answer lies in a combination of how businesses are valued and how investors behave.

The intrinsic value of a business is determined by its long-term earning power – a figure that moves slowly and is largely indifferent to the noise of day-to-day markets. Share prices, however, move constantly, driven by sentiment, short-term news flow and the collective tendency of investors to extrapolate recent experience into the future. When pessimism takes hold – as we explored in our last newsletter – prices can fall well below intrinsic value. When enthusiasm turns to euphoria, and investors crowd into fashionable areas, they can run well ahead of it.

It is this wedge between price and value that value investors seek to exploit, and it cuts in both directions. The discipline applies as much to knowing what to avoid as to knowing what to own.

The reason this opportunity persists is that the behavioural tendencies that create it keep recurring. The specific mis-pricings they produce are temporary – that is the whole point. But the human instincts that generate them – the discomfort of buying what others are selling, the allure of crowding into what everyone else is buying – are not. That discomfort is real. But historically, it has been the source of consistent outperformance.

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

— Benjamin Graham

The decade that proved the rule

Which brings us to the exception. The 2010s were, by any historical measure, an unusual decade for financial markets. In the aftermath of the global financial crisis, central banks around the world held interest rates at historically low levels for an extended period, while successive rounds of quantitative easing flooded markets with liquidity. These conditions had a profound effect on investor behaviour.

When the cost of money is close to zero, the present value of future cashflows – even very distant ones – appears to rise dramatically. This mechanical effect made growth companies, whose investment case rests heavily on earnings expected many years into the future, look extraordinarily attractive. The steady, cash-generative businesses that value investors tend to favour looked comparatively dull. Capital flowed accordingly – not because the underlying economics had changed, but because the unusual monetary environment had distorted the lens through which investors were looking.

The result was a decade in which the normal relationship between price and value was suspended. Not broken – suspended. Investors were not wrong to observe that growth was outperforming – we assert that they were wrong to conclude that this represented a new and permanent state of affairs. A century of evidence suggested otherwise, and so it has proved.

“The four most dangerous words in investing are: ‘This time it’s different.’”

— Sir John Templeton

Value reasserts itself

Since around 2021, as inflation returned and central banks began to raise rates, the conditions that had suppressed value’s relative performance have gradually unwound. As we explored in some detail in our October 2024 newsletter, value stocks have reasserted their historical dominance across the UK, Europe and Japan – and since that piece was written, the evidence suggests the US has begun to follow suit.

None of this should be surprising. The conditions of the 2010s were historically unusual. Their unwinding was always likely to restore the longer-run relationship between price and value that a century of evidence describes. What is perhaps most notable is how little attention this restoration has received – a reminder, if one were needed, of how quickly markets move on from the narratives they were once certain about.

“Value investing will always be relevant. To succeed, always buy for less than what it is worth, and be smarter than the market. It will never go out of style.”

— Charlie Munger

The next hundred years

As Temple Bar enters its second century, the world looks, as it always does, uncertain. Conflict in Iran is weighing on markets, inflation has proved stickier than many had hoped, and the interest rate cuts that investors were anticipating at the start of the year look less certain than they did. These are not trivial concerns.

But they are also not new ones. The history we have traced in this article is, in large part, a history of uncertainty – of investors navigating wars, crashes, bubbles and crises, and of a simple discipline repeatedly vindicating itself on the other side. It is worth noting that Temple Bar itself was founded at a moment of considerable economic turbulence, and that Nick and I were appointed as managers at what proved to be the peak of growth’s dominance. In both cases, the principles of value investing provided a reliable compass.

The lesson is not that uncertainty doesn’t matter. It is that uncertainty, and the anxiety it produces, is often precisely what creates the conditions in which value investing thrives.

“It is largely the fluctuations which throw up the bargains and the uncertainty due to the fluctuations which prevents other people from taking advantage of them.”

— John Maynard Keynes

One hundred years of evidence is a rare thing in financial markets. We do not take it lightly, and we do not think it should be dismissed. The principles that Benjamin Graham first set down in the 1930s remain, in our view, the most intellectually coherent framework for navigating whatever comes next. At Temple Bar, they remain the foundation of everything we do.

Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so.

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Nothing in this document should be construed as advice and is therefore not a recommendation to buy or sell shares. Information contained in this document should not be viewed as indicative of future results. The value of investments can go down as well as up.

This article is issued by RWC Asset Management LLP (Redwheel), in its capacity as the appointed portfolio manager to the Temple Bar Investment Trust Plc. Redwheel is authorised and regulated by the UK Financial Conduct Authority and the US Securities and Exchange Commission.

The statements and opinions expressed in this article are those of the author as of the date of publication.

Redwheel may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. Redwheel seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is directed only at professional, institutional, wholesale or qualified investors. The services provided by Redwheel are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.

The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by Redwheel; or (iv) an offer to enter into any other transaction whatsoever (each a Transaction). No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party. Redwheel bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction.

How to Invest

The Company’s shares are traded openly on the London Stock Exchange and can be purchased through a stock broker or other financial intermediary.